We ran cost analyses for multiple cases. Here are two of the most interesting cases. Case 1 is a cost analysis for production, showing relative costs of different aspects of manufacturing. Case 3 is the same plot except for mass production through a rented manufacturing line, such as through companies like Protomold.

|

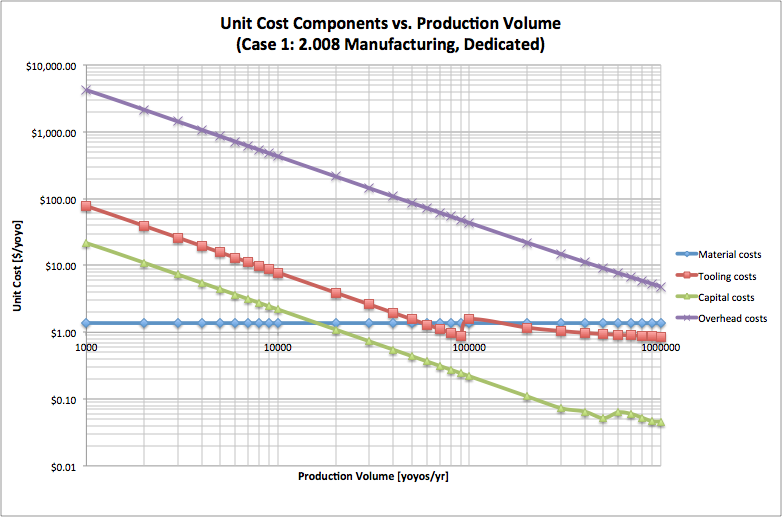

| Figure 1: Cost analysis for prototyping in 2.008 |

The first graph confirms that unit cost decreases (very steeply at first, before leveling off) as production volume increases, and the second graph tells us that this relationship is due to drops in the tooling, capital, and overhead costs. The unit material costs remain constant since we are allowed to purchase just the right amount. As our volume increases, the unit tooling cost decreases, which is just what we would expect because the same mold is getting used for more runs. In other words, the cost of making that mold doesn’t increase, but it gets divided by a larger number of produced parts when we calculate the unit cost. At 100,000, however, the tooling cost jumps up for a data sample because we have to pay for the tooling of new mold sets (we assumed mold life of 100,000). The overhead cost is the largest contributor to the total manufacturing cost. It decreases as volume increases because a smaller percentage of the dedicated machines/employees are being paid for “wasted” time. Capital costs decrease with increasing volume because

|

| Figure 2: Cost analysis for mass production |

As we saw before in case (1), volume has no effect on the material costs; if you make more parts, you need to buy exactly much more material. Here, the overhead costs remain constant at $1.36 per yoyo because Case (3) calls for a rented manufacturing line. This means that employees and machines are both non-dedicated. Since we already don’t pay for any “wasted” time in the overheads at low volume, increasing production volume does not lead to more efficient use of workers and machines. Similarly, capital costs remain constant at $0.04 because the machines are already operating at full capacity. Tooling costs still decrease with increasing production volume; the rented line has no bearing on tooling, because we still need to machine all the mold sets. And then again we can see the little upward “blip” in the downward trend of the tooling cost, specifically at 100,000 yoyos. This is due to the added tooling expenses of making more mold sets for each yoyo part, since we assumed mold life to be 100,000 runs.

No comments:

Post a Comment